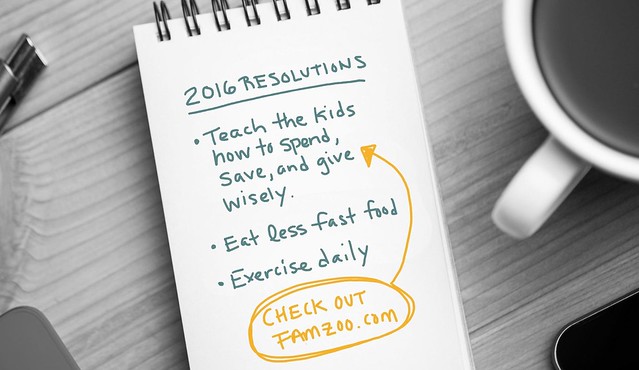

What does your list of resolutions for 2016 look like? Something like this?

Eat less fast food.

Exercise more.

Teach the kids good money habits.

Sorry, you’re on your own for the first two. But I can help you nail number three.

How? I’ve been collecting tips throughout the year from the best family finance articles on the Internet. I’ve listed my favorite ones below. Just circle a few tips that make the most sense for your kids, and pop them on your list.

That’s right. No kid is going to hate you for handing over cold hard cash as a present this holiday season. The same holds for gift cards, as long as you get the brand right. That might be a little trickier than you think, judging by the billions of dollars worth of unused gift cards floating around out there.

And while cash and gift cards aren’t the most imaginative gifts, at least some folks get pretty darn creative on the packaging. Maybe you can even try your hand on some clever money origami this year.

Still, wouldn’t you feel a bit more thoughtful giving a financial gift that isn’t purely focused on immediate consumption? Perhaps something a bit longer term and, dare I say, educational?

I know what you’re thinking. Yawn. But bear with me, I’ve got some cool options that are worth your consideration.

Your kids know how to stack blocks, but do they know how to stack bills? How about 100 dollar bills? You know, the “Benjamins.”

They will if you listen to last Friday’s episode of the popular personal finance podcast Stacking Benjamins. The host, Joe Saul-Sehy, invited me to join fellow panelists Len Penzo and Tai McNeely in a lively round-table discussion on teaching kids good money habits. Joe plucked a range of topics from three recent articles.

Here’s an outline of the discussion with the 29 key points and tips. Check out the timeline if you want to jump right to your favorite spots in the podcast:

I have a shortlist of healthy habits I’d like to instill in my kids, and charitable giving is definitely

on it. It’s right up there with a solid work ethic and regular exercise. In fact, charitable giving has

a lot in common with exercise:

Nobody else can do it for you.

It can be tough to get started.

You always feel good about it afterwards.

You might even argue that charitable giving is better than exercise because it makes other

people feel good too.

So how can you motivate your child to get started with charitable giving and, ideally, turn it into a

life-long habit? Here are six approaches that have worked well with our kids so far.

“Which business best addresses a consumer personal finance or investing problem?”

That was the question posed to 900+ FinCon15 attendees via a mobile polling app. The outcome would determine the winner of the People’s Choice Award at the annual FinTech Startup Competition.

The people spoke: FamZoo. Woot!

I can’t tell you how gratifying it is to earn the respect of the FinCon community for our efforts to improve the financial capability of kids and teens — and, surreptitiously, parents too! Here’s an audience who lives and breathes the personal finance challenges that everyday people face. Their opinion is a tremendous validation of the FamZoo mission and efforts to date.

But what about the formal competition judges? James Ray of Chase Merchant Services, Rachel Schneider of the Center for Financial Services Innovation, Dan Roselli of Packard Place, and J. Money of Budgets Are Sexy. What did they think?

They mulled over the following formal judging criteria:

Has the summary/presentation clearly articulated the value proposition?

Has the summary/presentation demonstrated market opportunity?

Has the summary/presentation demonstrated a sustainable business model that will make money, or, in the case of a venture with a social purpose, make money and have the desired social impact?

Has the summary/presentation demonstrated competitive differentiation/intellectual capital?

How effective was the overall presentation?

Would you invest or back this opportunity?

The judging panel spoke too: FamZoo. And TickerTags. A tie for first.

A tremendous honor, and a nice check to boot!

But what about you? What do you think?

Here’s an informal Periscope broadcast where I walk through an extended version of the demo.

The FinCon people have spoken. The judges have spoken. What say you?

P.S. Several folks have asked us how we plan to use the money. We always coach families to split income between important buckets like spending, saving, investing, and giving. That’s sound advice for families and companies alike, so we’re taking it ourselves. Here’s the game plan:

50% to spending: We have some immediate needs to address in our iPhone app, so we’re going to spend $3,000 on a dedicated iPhone development resource right away.

16.6% to saving: You never know when that next unanticipated expense is going to pounce! $1,000 is going in our “Emergency Fund” for the next thing to hit the fan.

16.6% to investing: Smart investing often entails having “dry powder” available to jump on an opportunity. We’re parking $1,000 to deploy on the next serendipitous growth partnership that comes our way.

16.6% to giving: FamZoo’s “secret ulterior motive” is to jumpstart the lifelong habit of philanthropy, and we like to walk the talk in this department too. We favor charitable missions that are tightly aligned with our own. That’s why we’re donating $1,000 to the fledgling Plutus Foundation to help bring financial capability to those who need it most.

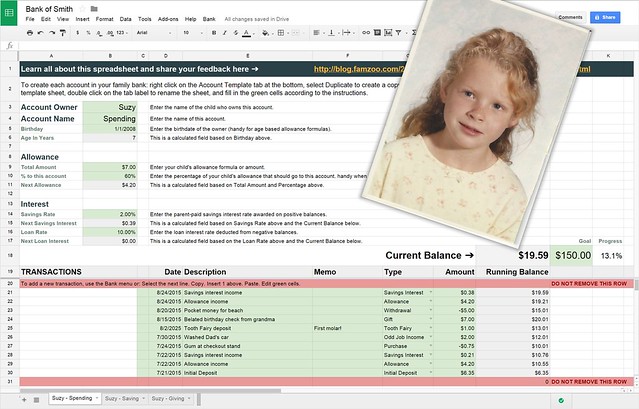

Let’s face it. Your kid’s piggy bank isn’t cutting it any more.

Sure, it was a fine first introduction to the most rudimentary concepts of money, but your kid is a smart cookie. Basic lessons learned.

So when are you going to take your kid’s money IQ to the next level? Your youngster is perfectly capable of grasping the following and more:

How bank accounts work.

How to track income and spending as numbers instead of coins.

How to avoid costly debt.

How to put money to work with compound interest.

How to allocate money to specific financial goals.

That sounds like a daunting parental task, but it doesn’t have to be.

You can do it all with a simple spreadsheet. That’s how I started out with my kids, and I’m not alone. The wildly popular financial blogger Mr. Money Mustache is doing the same. He’s using his “Bank of Mr. Money Mustache” spreadsheet to teach his young son about money too.

What’s the best way to teach your youngster about saving and the power of compound interest?

Everybody knows you march your kid straight down to the local bank or credit union and open up a traditional savings account. Right? That’s certainly the conventional wisdom.

In fact, opening a savings account for your 6 year old is the “official” wisdom too. So says the panel of financial experts who make up the United States President’s Advisory Council on Financial Capability. It’s item 8 on their list of 20 things kids need to know to live financially smart lives.

My take? That’s complete bullcorn.

Let’s just think about this from a 6 year old’s perspective for a moment:

Maybe parents have lots of questions about kids and saving, but they’re just afraid to ask.

That’s why we took to the Twittersphere with our friends @GiftOfCollege earlier this month. We posed 9 key questions about teaching kids to save, starting with the most basic: why?

Here are the 9 questions and an edited summary of the top answers.

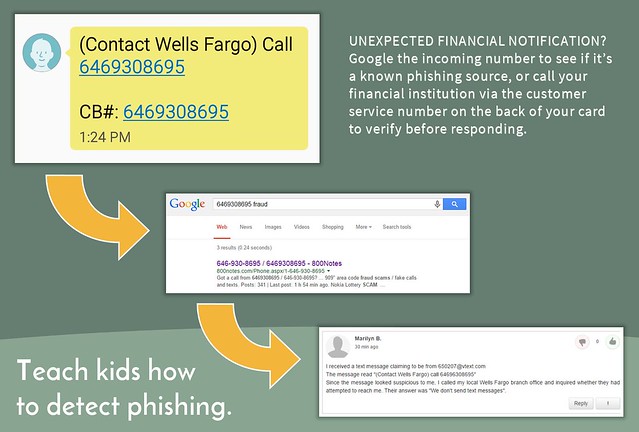

Do your kids have access to email or text messages?

Then it’s time to teach them about “phishing” — sneaky attempts to extract sensitive personal information like usernames, passwords, account numbers, etc.

For example, suppose your child gets the following text message out of the blue:

How can we as parents know we’re teaching our kids the right things about money? That’s a tough question. There’s lots of potential ground to cover, and it can be hard to cull out what’s truly important.

What if you could jump in a time machine, set the dial forward 25 years, blast into the future, and ask your children — now grown adults — what they wish they had learned from you about money? Answers in hand, you could just travel back in time and make sure you carefully covered those bases.

Obviously, that’s not going to happen, but I might have the next best thing for you. What if you could corral a whole bunch of thoughtful, accomplished, even famous adults and collect their answers to the following question:

Joe Saul-Sehy hosts one of the most popular podcasts in the personal finance space. It’s called Stacking Benjamins, and it’s been at the top of my Stitcher favorites list for weeks now. Joe and his co-hosts magically transform normally bland finance and investing topics into chuckle-worthy entertainment. That’s no small feat. When was the last time you caught yourself guffawing over qualified retirement annuities? Yeah, never.

Needless to say, I’m a huge Stacking Benjamins fan. So, when Joe emailed me a couple weeks ago to be on the show, I was beyond thrilled.

As preparation for the show, Joe asked me to think about “horrible ways to deploy allowance.” I jotted down 5 favorites that sprung to mind. Here’s my list (accompanied by some handy justifications for parents who are determined to stay the course):

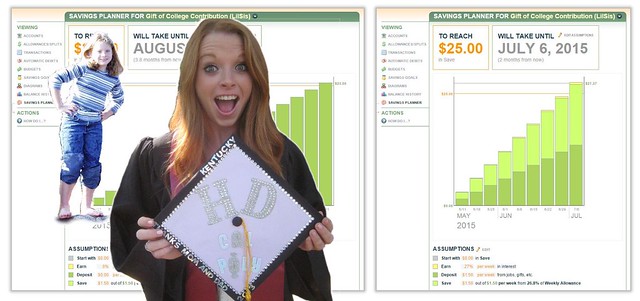

How in the world can a 6 year old making in the neighborhood of $6 a week contribute meaningfully to a college savings fund? Easy. A “micro-savings” card, a split, and a Gift Of College account will do the trick.

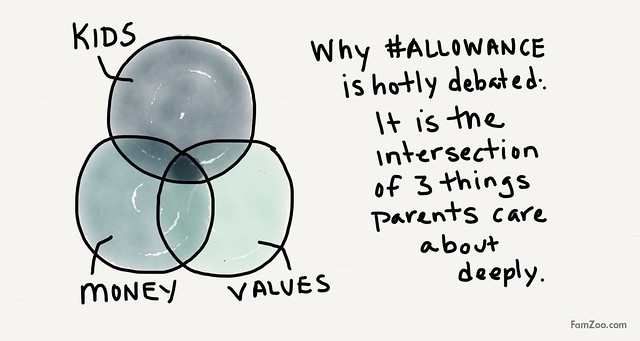

Want to spark an animated debate? Just broach the topic of allowance in a room full of parents. Allowance is one of those hot button words that never fails to elicit passionate opinions. That’s because it stands at the volatile intersection of three things parents care deeply about: money, kids, and values.

So we’re bringing parents from across the twittersphere together into one big virtual room to really stir things up! FamZoo and The Centsables are hosting an #Allowance chat on Twitter to mark the final week of National Financial Literacy Month. Join us and a tweet-load of other passionate parents on Tuesday, April 28th at 9am Pacific / noon Eastern time.

We’ll be discussing the following 10 classic questions about allowance:

Is that the extent of the “discussion” you have with your kids about taxes each year?

You’re not alone. Most of us send exclusively negative tax messages to our kids with our subtle or not-so-subtle demeanor throughout the filing season. At minimum, kids in a typical family might overhear an expletive or two (or ten!) reverberating throughout the house in the days leading up to the universally despised April 15th deadline.

Expletives aside, have you ever taken the time to really explain what taxes are all about? Can you blame your kid for thinking that taxes are just some vague evil thing that make mom and dad grumpy? We’re doing our kids a disservice when we keep them in the dark about the what and why of taxes and how to handle them. Need more convincing? Check out Neale Godfrey’s thoughtful piece in Forbes: Life Is Taxing... Teaching Your Kids Real Financial Facts.

Here are a few ideas for shedding some light on taxes for your kids:

Perhaps you’ve heard of behavioral economics — the study of the role psychological, social, cognitive, and emotional factors play in economic decisions. It explains why we’re such suckers for those cleverly worded BOGO offers and other sneaky marketing tricks. Our emotions, stereotypes, and rules-of-thumb interfere with our ability to make strictly logical financial decisions.

But what about our genetic makeup? How do our genes influence our financial decision making? That’s what the emerging field of neuroeconomics is all about. Can you blame your kid’s lousy money behavior on his 5-HTTLPR gene? Maybe a little. Check out Your Genes Might Affect Your Credit Score to see how a Stanford University study linked variations in a specific gene to riskier financial decisions and lower FICO scores.

We all want to raise kids who are grounded, generous, and smart about money, right?

Yep. Just show us the manual!

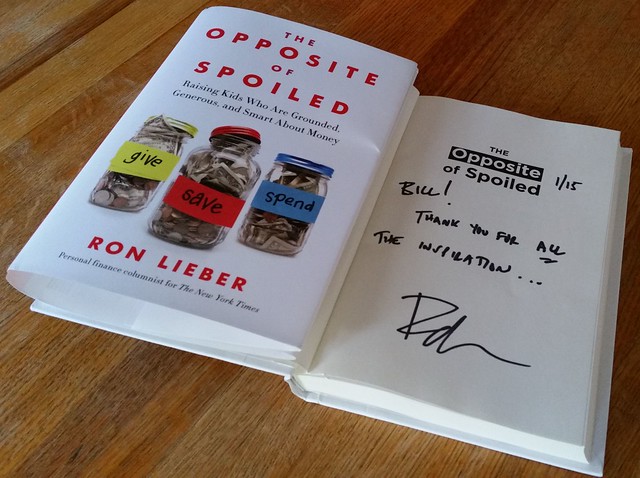

Well, as of last week, you can pick up an excellent one courtesy of Ron Lieber, the personal finance columnist for The New York Times. It’s called The Opposite of Spoiled.

Apparently, spending like a pop star finally caught up to “the responsible teen spending company.” Today marked the formal end of the teen prepaid card programs offered by SpendSmart Networks, Inc. and endorsed by none other than teen idol and dubious financial role model, Justin Bieber.

I love this article about a dad who pays his son’s allowance in Bitcoin using a service called ChangeTip. Check out the post Why I Pay My 7th Grader’s Allowance in Bitcoin. Gil explains how he does it and why. It’s as much about father-son bonding and education as it is about money.

I dig the approach, but you have to be willing to jump into the brave new world of Bitcoin which is still fairly daunting and somewhat sketchy in my opinion. Here’s a good place to start if you’d like to see what’s involved: Getting Started with Bitcoin from the Bitcoin Foundation.

Here are the rest of my favorite family finance picks from the month of December.